India Prepaid Cards Market Size, Share, Trends and Forecast by Card Type, Purpose, Vertical, and Region, 2026-2034

India Prepaid Cards Market Size, Share, Trends & Forecast (2026-2034)

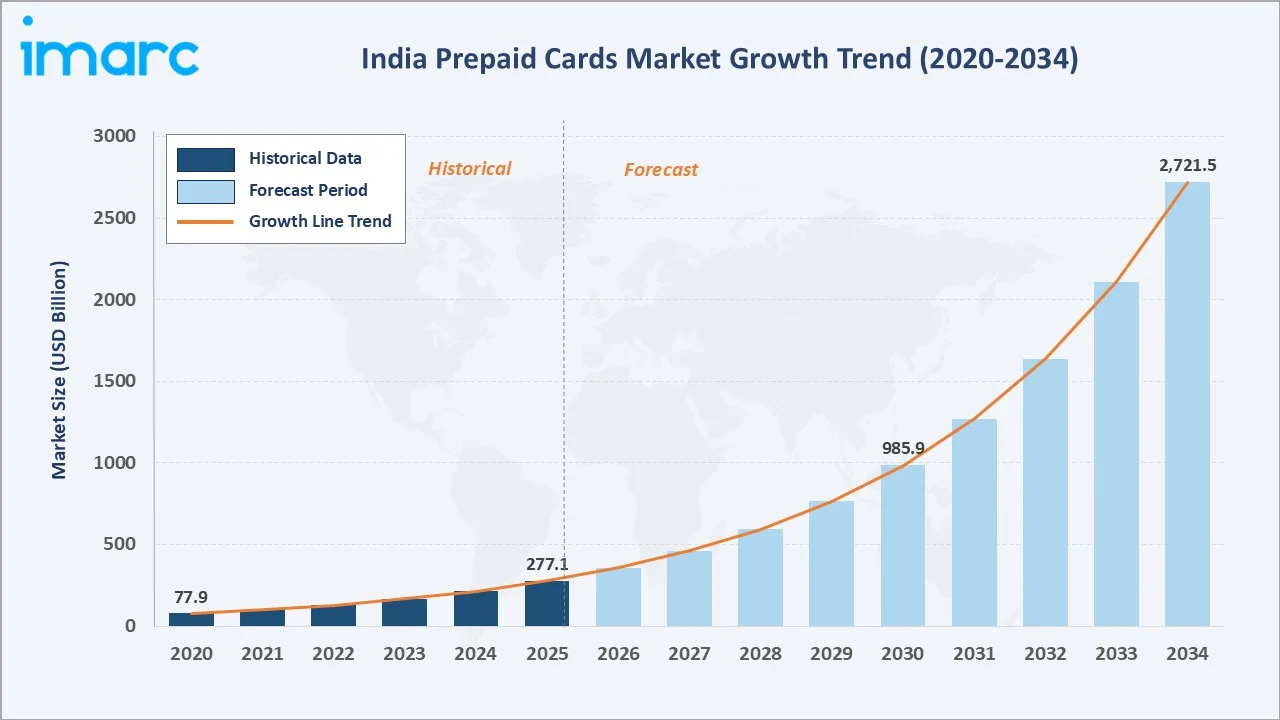

The India prepaid cards market reached USD 277.1 Billion in 2025 and is projected to reach USD 2,721.5 Billion by 2034, growing at a CAGR of 28.9% during 2026-2034. Market growth is fueled by India's accelerating digital payment ecosystem, government financial inclusion programs, UPI infrastructure integration, rising corporate expense management adoption, and expanding e-commerce enabling prepaid instruments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 277.1 Billion |

|

Forecast Market Size (2034) |

USD 2,721.5 Billion |

|

CAGR (2026-2034) |

28.9% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

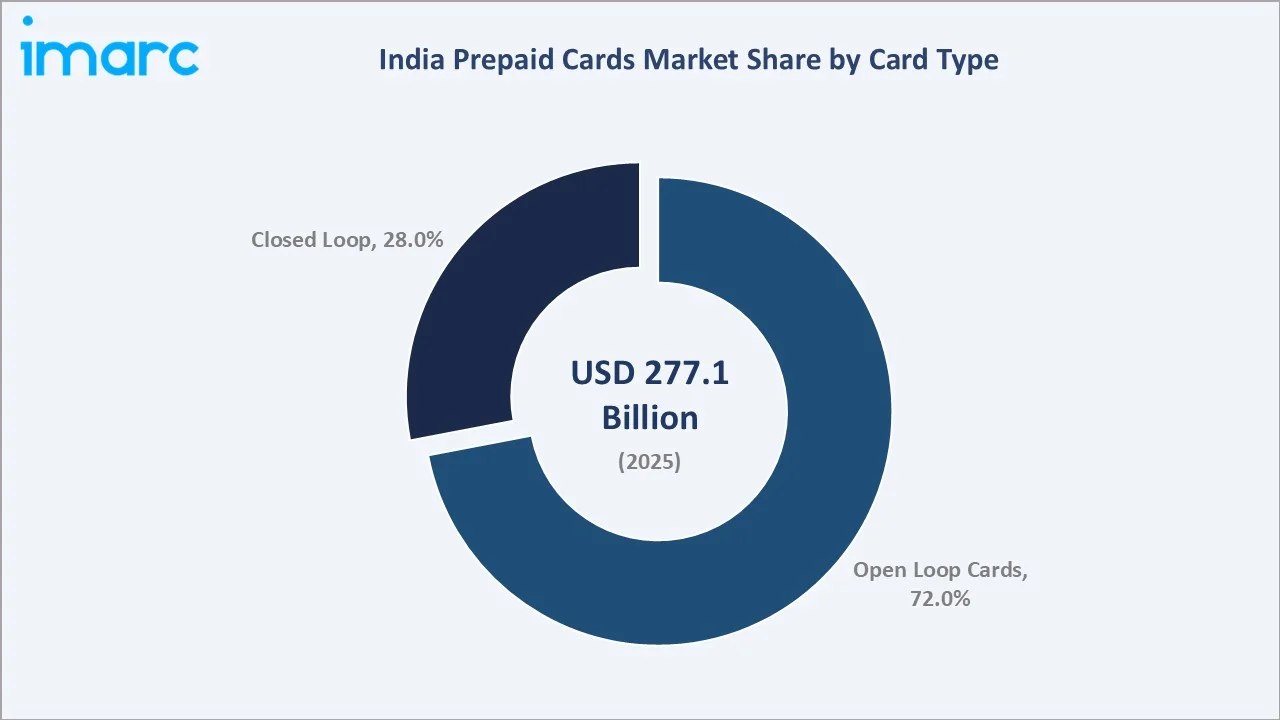

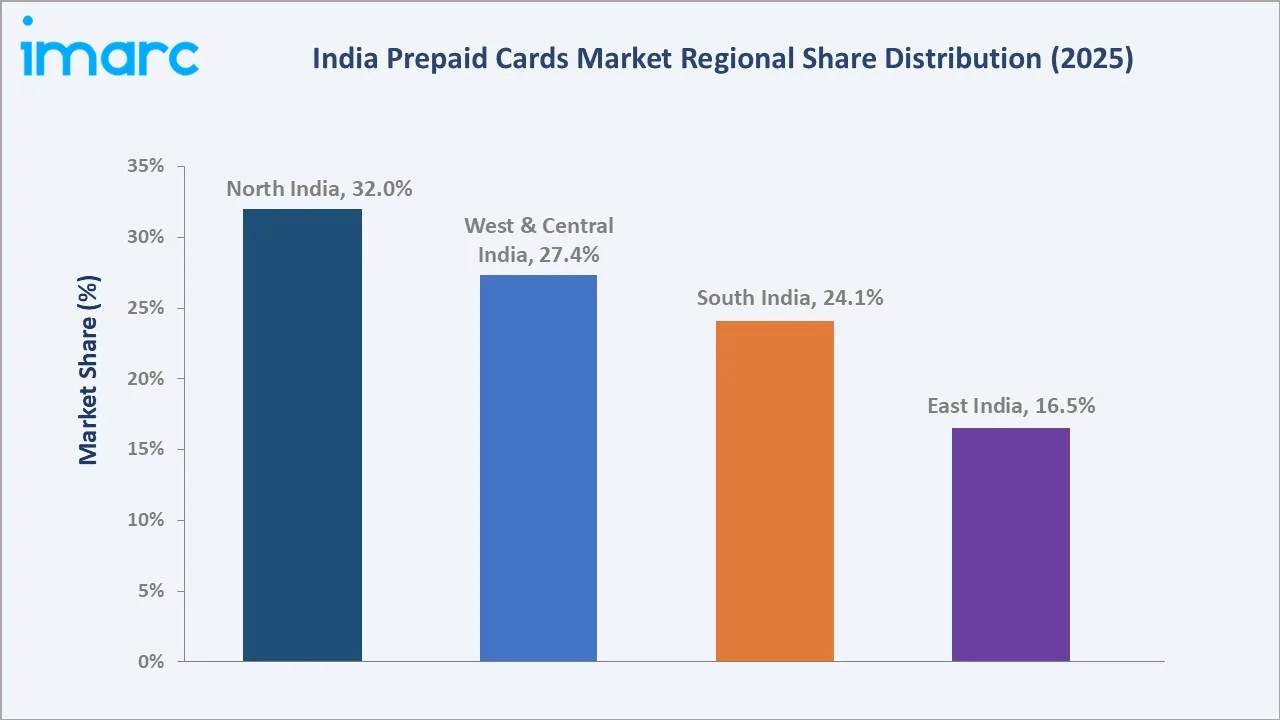

North India's 32.0% market leadership reflects Delhi-NCR's status as India's largest concentration of corporate headquarters, government ministries, and high digital payment adoption. Open loop cards' 72.0% dominance reflects the Visa/Mastercard/RuPay network infrastructure that enables acceptance at millions of merchant points nationally, making them substantially more versatile than closed loop cards.

To get more information on this market, Request Sample

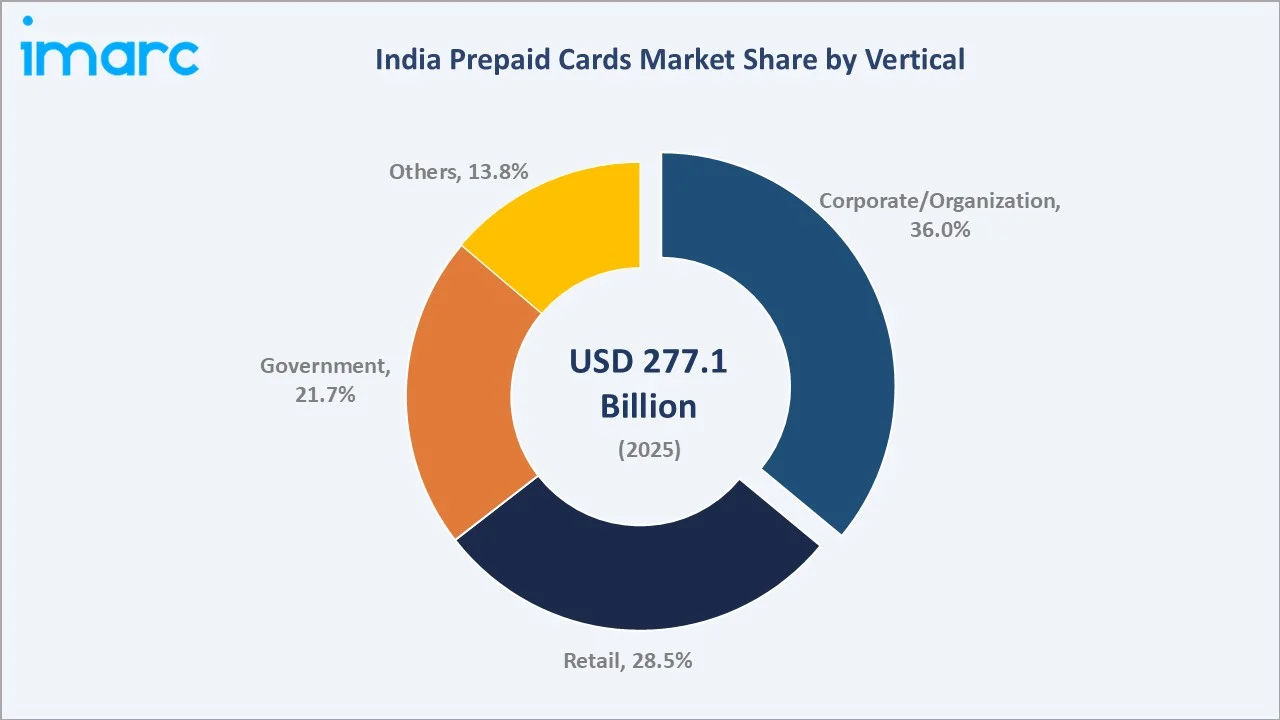

Corporate/organization at 36.0% reflects the growing enterprise adoption of prepaid cards for payroll, travel, and expense management programs. The market's exceptional 28.9% CAGR is driven by India's structural shift from cash to digital payments, accelerated by demonetization’s legacy, COVID-19's contactless payment push, and the government's sustained Digital India and BharatNet connectivity investments.

Executive Summary

The India prepaid cards market is among the fastest-growing fintech-adjacent market segments in India, experiencing near-exponential volume growth as digital payment adoption becomes mainstream across retail, corporate, and government sectors. From USD 277.1 Billion in 2025, the market will reach USD 2,721.5 Billion by 2034, generating USD 2,444.4 Billion in incremental value at a 28.9% CAGR.

Open loop cards lead at 72.0%, leveraging Visa, Mastercard, and RuPay global and domestic payment networks for universal merchant acceptance. Corporate/organization is the largest vertical at 36.0%, driven by companies adopting prepaid cards for payroll disbursement to unbanked workers, travel allowances, business expense management, and incentive distribution programs that replace paper-based vouchers and cash disbursements.

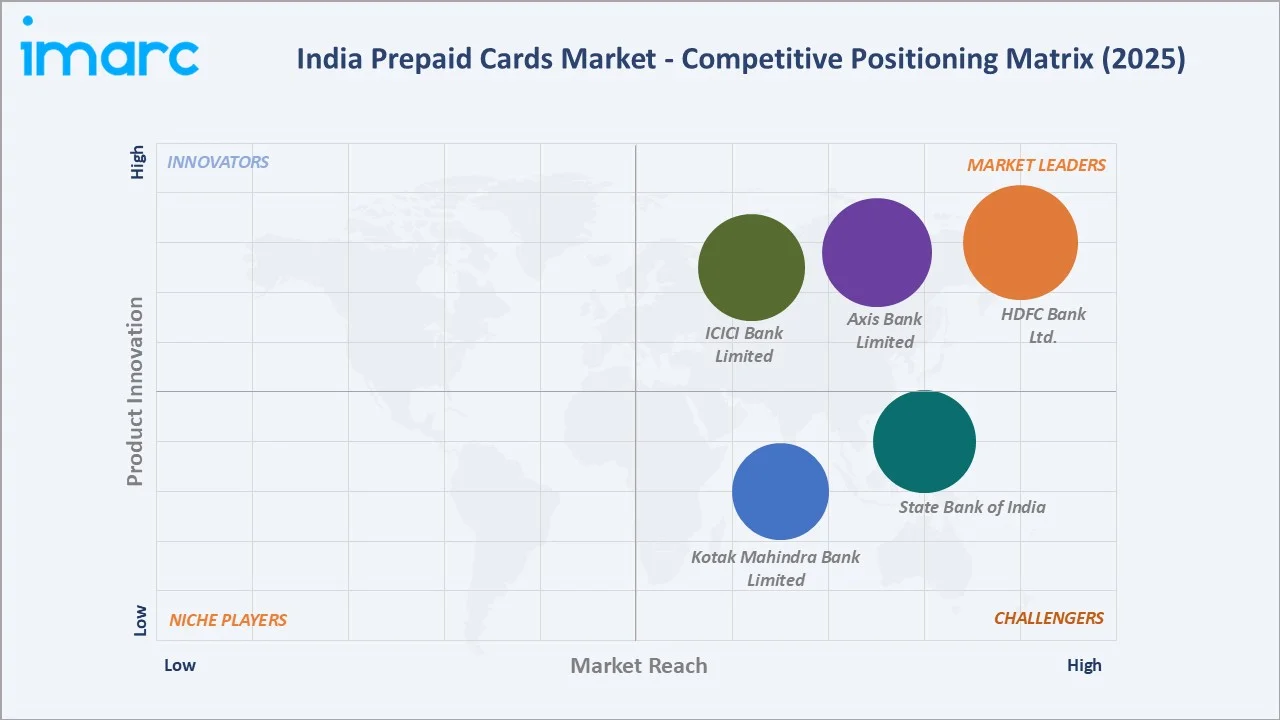

Key players, including HDFC Bank Ltd., Axis Bank Limited, ICICI Bank Limited, State Bank of India, and Kotak Mahindra Bank Limited, compete through card program innovation, digital wallet integration, corporate client servicing, and distribution network breadth across India's diverse geography.

Key Market Insights

|

Insight |

Data |

| Largest Card Type | Open Loop Cards – 72.0% share (2025) |

| Second Largest Card type | Closed Loop Cards – 28.0% (2025) |

| Largest Vertical | Corporate/Organization – 36.0% share (2025) |

| Second Largest Vertical | Retail – 28.5% (2025) |

| Leading Region | North India – 32.0% share (2025) |

| Top Companies | HDFC Bank Ltd., Axis Bank Limited, ICICI Bank Limited, State Bank of India, and Kotak Mahindra Bank Limited |

Key Analytical Observations:

- Open loop cards at 72.0% (2025) are dominant because their network acceptance across Visa, Mastercard, and India's RuPay domestic payment scheme enables usage at any POS terminal, ATM, and e-commerce checkout nationwide.

- Corporate/organization at 36.0% (2025) is the market's largest and most strategically important vertical. Indian enterprises are replacing cash salary disbursements and paper expense vouchers with prepaid corporate cards that provide real-time expense visibility, automated reconciliation, and compliance documentation.

- Government at 21.7% (2025) represents the fastest-growing structural demand segment as the Indian government digitizes benefit disbursements. Jan Dhan Yojana direct benefit transfers (DBT), MGNREGS wage payments, and state government welfare transfers are progressively being channeled through prepaid instruments linked to Aadhaar-authenticated beneficiary accounts.

- Retail at 28.5% (2025) serves consumer-facing prepaid card use cases, including general purpose reloadable (GPR) cards for everyday spending by the underbanked, gift cards for gifting occasions replacing paper gift vouchers, forex travel cards for international travelers offering multi-currency loading, and transit cards for metro and bus networks.

India Prepaid Cards Market Overview

Prepaid cards are payment instruments that allow users to load a predetermined amount of funds that can be spent at merchant locations, online platforms, ATMs, or for fund transfers, without requiring a traditional bank account linkage.

In India, prepaid cards are regulated as Prepaid Payment Instruments (PPIs) by the Reserve Bank of India (RBI) under the Payment and Settlement Systems Act, 2007, and the Master Direction on Prepaid Payment Instruments (2021).

India's prepaid card ecosystem has undergone a fundamental transformation since demonetization in 2016, accelerated by the UPI digital payment infrastructure's expansion, the COVID-19 pandemic's shift to contactless payments, and the government's progressive digital financial inclusion agenda.

The RBI's 2021 PPI Master Direction significantly liberalized the prepaid card regulatory framework, enabling interoperability of wallets, expanding permissible transactions, and creating a level playing field between bank-issued and non-bank PPI products, which catalyzed a new wave of corporate and consumer prepaid card program launches.

Market Dynamics

To evaluate market opportunities, Request Sample

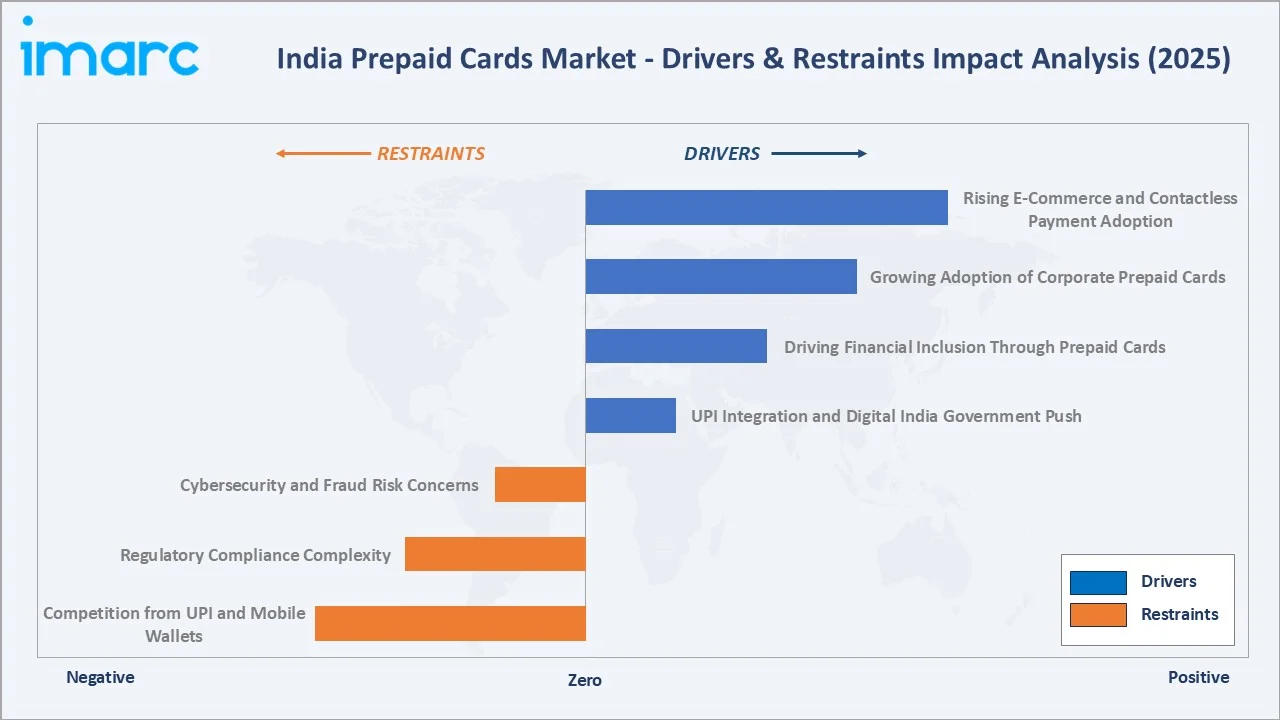

Market Drivers

- UPI Integration and Digital India Government Push: India's Unified Payments Interface (UPI) annual transaction volume surged from just 2 crore transactions in FY 2016–17 to more than 24,162 crore transactions in FY 2025–26. The RBI's mandate for interoperability of PPIs has massively expanded the merchant acceptance universe for prepaid cards to include all 350+ million UPI-enabled merchants in India.

- Driving Financial Inclusion Through Prepaid Cards: According to the World Bank, nearly 190 million adults in India remain without access to formal bank accounts. Prepaid cards serve as an accessible financial inclusion instrument providing digital payment capability, online shopping access, and formal financial ecosystem participation.

- Growing Adoption of Corporate Prepaid Cards: Enterprises are adopting prepaid corporate cards for payroll, travel, fuel, and expense management. Construction, logistics, FMCG, and manufacturing companies use payroll prepaid cards for contract workers lacking bank accounts.

- Rising E-Commerce and Contactless Payment Adoption: India's e-commerce market exceeded USD 129.72 Billion in 2025, growing at a compound annual growth rate of 19.63% from 2026 to 2034. This creates an expanding demand for prepaid card instruments that enable online transactions by users without credit cards.

Market Restraints

- Cybersecurity and Fraud Risk Concerns: RBI's two-factor authentication requirements and card network fraud monitoring systems have reduced fraud incidence, but consumer awareness of prepaid card security limitations relative to credit cards constrains adoption in fraud-sensitive segments.

- Regulatory Compliance Complexity: Banks and non-bank PPI issuers must comply with RBI's KYC/AML requirements, PMLA reporting obligations, IT security standards, and customer grievance redressal framework. Minimum detail PPI issuers face simpler KYC requirements but are restricted in functionality, while full KYC PPI programs require complete KYC documentation processing that adds onboarding friction for potential users.

- Competition from UPI and Mobile Wallets: India's UPI system and mobile wallet ecosystem offer many of the same financial inclusion and digital payment benefits as prepaid cards at a lower cost and with a simpler user experience.

Market Opportunities

- Neobank and Fintech Prepaid Card Platform Development: India's growing neobanking and fintech ecosystem is building differentiated prepaid card products with AI-personalized rewards, real-time spending analytics, instant virtual card issuance, and seamless UPI integration.

- Government Benefit Disbursement Digitalization: According to a quantitative assessment by the BlueKraft Digital Foundation, India’s Direct Benefit Transfer (DBT) system has generated cumulative savings of INR 3.48 lakh crore by reducing leakages in welfare delivery.

Market Challenges

- Low Cardholder Engagement and Abandonment Rates: Studies of prepaid card programs in India consistently show high initial activation rates but significant drop-off in ongoing usage, as consumers default to UPI or cash for everyday transactions after initial prepaid card trials.

- Merchant Acceptance Cost Barriers for Small Merchants: Merchant discount rate (MDR) waiver on RuPay debit and UPI transactions has distorted merchant acceptance economics, making UPI acceptance economically preferable for small merchants versus prepaid card acceptance that still attracts MDR costs in some configurations.

Emerging Market Trends

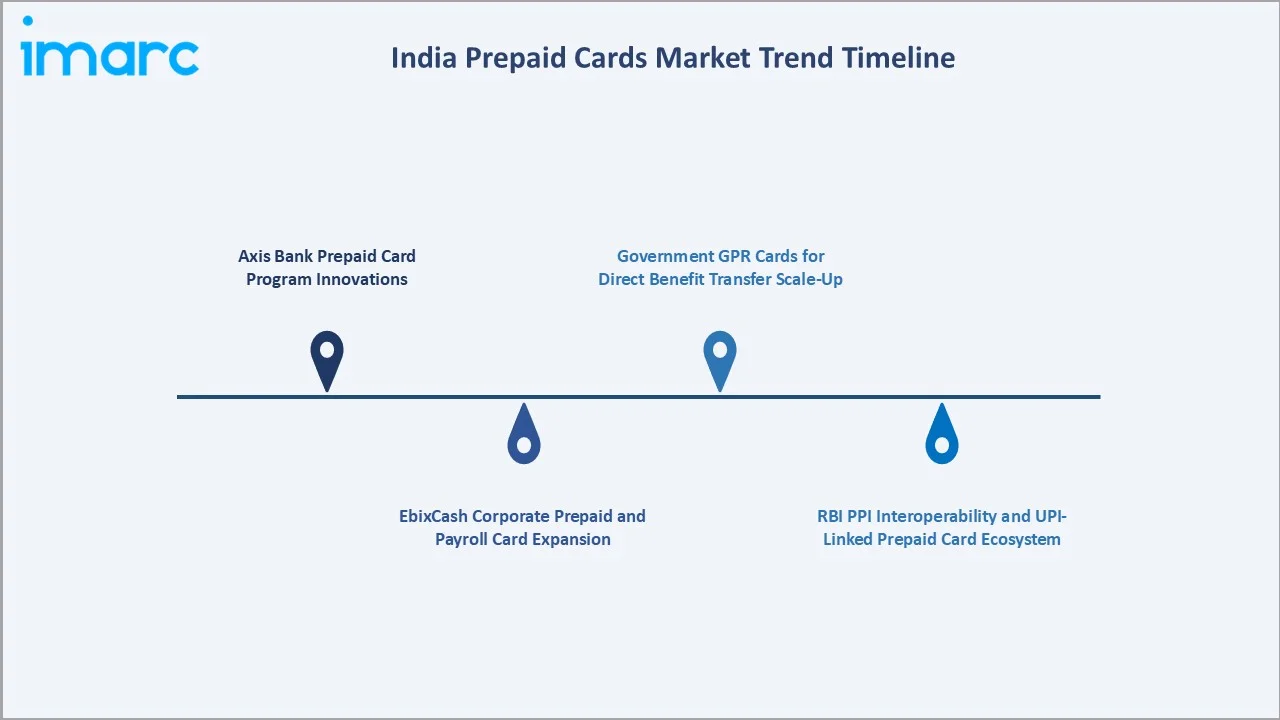

1. Axis Bank Prepaid Card Program Innovations

Axis Bank has expanded its Visa-powered prepaid gift card and travel card programs, integrating them with its mobile banking app for seamless digital loading, real-time transaction alerts, and instant virtual card generation. In May 2024, Axis Bank collaborated with Mastercard to introduce the NFC Soundbox, an all-in-one merchant payment device supporting Bharat QR, UPI, Tap & Pay, and Tap + Pin transactions.

2. EbixCash Corporate Prepaid and Payroll Card Expansion

EbixCash expanded its enterprise client base for payroll disbursement cards, travel prepaid cards, and employee meal voucher cards. EbixCash's platform integrates with major HRMS and payroll software systems, enabling automated payroll card loading and multi-purse card management.

3. RBI PPI Interoperability and UPI-Linked Prepaid Card Ecosystem

The RBI's mandate for interoperability among PPI wallets and prepaid cards has fundamentally enhanced prepaid card utility by enabling balance transfers between different PPI issuers and allowing prepaid card balances to be transacted via UPI QR codes at any UPI-accepting merchant.

4. Government GPR Cards for Direct Benefit Transfer Scale-Up

India's DBT program has disbursed over INR 3.48 Lakh Crore since its inception. State governments in Madhya Pradesh, Rajasthan, Odisha, and Tamil Nadu issue dedicated prepaid cards for housing allowance, scholarship, and agricultural subsidy schemes, enabling controlled category spending while building long-term financial inclusion.

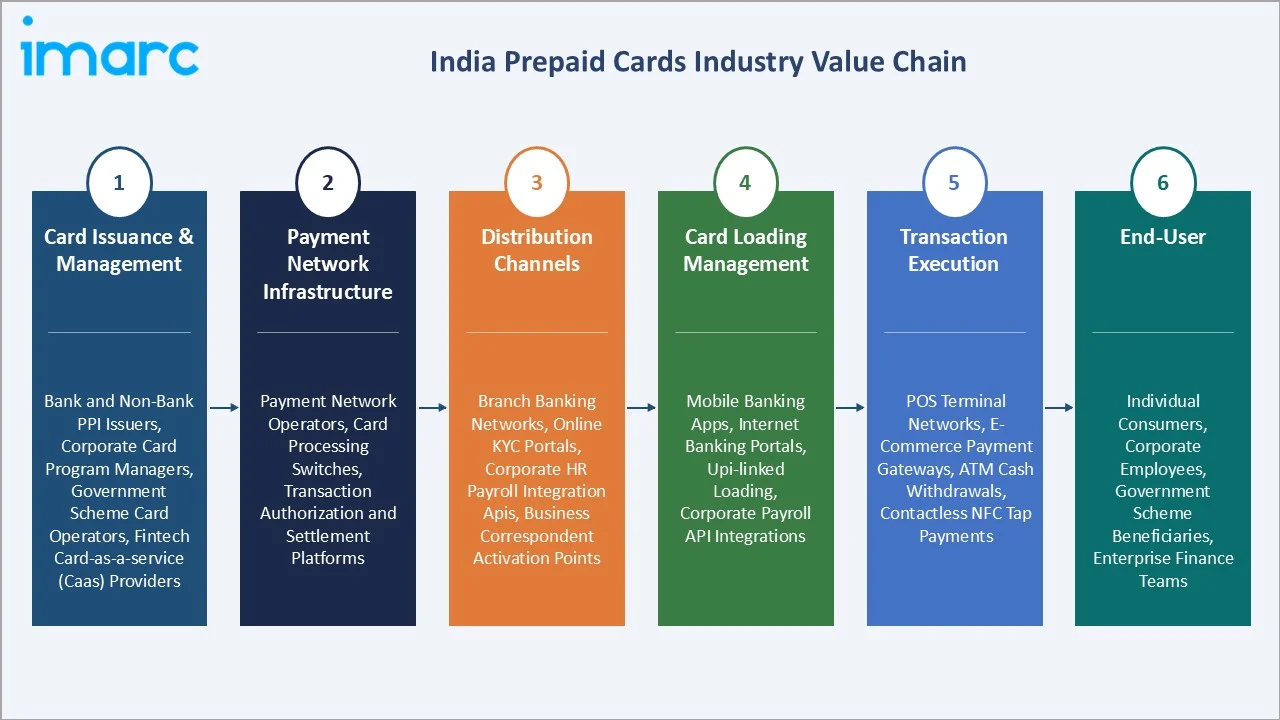

Industry Value Chain Analysis

India's prepaid card value chain spans card program management through payment network infrastructure, distribution, balance management, and end-user transaction processing, with increasing digital-first and API-driven service layers.

|

Stage |

Key Players / Examples |

| Card Issuance & Management | Bank and non-bank PPI issuers, corporate card program managers, government scheme card operators, fintech card-as-a-service (CaaS) providers |

| Payment Network Infrastructure | Payment network operators, card processing switches, transaction authorization and settlement platforms |

| Distribution Channels | Branch banking networks, online KYC portals, corporate HR payroll integration APIs, business correspondent activation points |

| Card Loading Management | Mobile banking apps, internet banking portals, UPI-linked loading, corporate payroll API integrations |

| Transaction Execution | POS terminal networks, e-commerce payment gateways, ATM cash withdrawals, contactless NFC tap payments |

| End-User | Individual consumers, corporate employees, government scheme beneficiaries, enterprise finance teams |

Technology Landscape in the India Prepaid Cards Industry

UPI Integration and Prepaid Card Interoperability

RBI-mandated PPI interoperability enables prepaid card balances to be linked to UPI IDs and transacted at any of 350+ million UPI-accepting QR code merchants. NPCI's PPI-to-bank account transfer capability enables beneficiaries to sweep prepaid balances to bank accounts. Bank-issued prepaid cards linked to UPI via mobile banking apps combine card swipe, NFC contactless, and QR-code scan in a single instrument.

API-Driven Corporate Card Program Management

Corporate prepaid card platforms use REST API integration with HRMS, ERP, and expense management software to automate card issuance, balance loading, and spend limit configuration. EbixCash's and Pluxee's platforms provide real-time spend dashboards across all employee card purses – meal, travel, fuel, and general, with automated GST invoice generation and direct integration with Tally, SAP, and Oracle ERP.

AI and ML-Based Fraud Detection and Risk Management

HDFC Bank and Axis Bank deploy ML-based transaction monitoring that flags unusual geographic patterns, rapid small transactions (card testing), and atypical merchant category spending for automated block or OTP verification. AI-driven velocity controls and device fingerprinting have significantly reduced prepaid card fraud rates across premium program categories.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Card Type | Open Loop Cards | 72.0% |

2025 |

| Vertical | Corporate/Organization | 36.0% |

2025 |

| Purpose | General Purpose Reloadable (GPR) Cards | 30.0% |

2025 |

|

Region |

North India |

32.0% |

2025 |

By Card Type

Open loop cards lead at 72.0% in 2025. Their universal acceptance on Visa, Mastercard, and RuPay networks across POS terminals, e-commerce platforms, and ATMs nationally and internationally makes them substantially more versatile than closed loop alternatives.

To access detailed market analysis, Request Sample

Closed loop cards at 28.0% serve ecosystem-bound use cases: corporate canteen/meal cards at designated vendors, metro and bus transit cards, campus cards at educational institutions, and loyalty cards redeemable within specific retail chains.

By Vertical

Corporate/organization at 36.0% is driven by enterprise payroll cards for contract workers, travel and expense management, fuel cards for fleet staff, and incentive cards for sales force programs. The Payment of Wages Act amendment, enabling digital wage payment, supports continued corporate vertical expansion.

Retail at 28.5% serves GPR, gift, forex, and transit card demand. Government at 21.7% is growing through the DBT program scale-up. Others (13.8%) include healthcare spending, education fees, and remittance cards. Government vertical share will expand as remaining cash welfare disbursements are digitalized.

Regional Market Insights

North India leads with a 32.0% market share in 2025. Delhi-NCR hosts the highest concentration of corporate headquarters, government ministries, and a large organized sector workforce, which drives both corporate and government prepaid card issuance.

West and Central India's 27.4% share is anchored by Mumbai's unique position as India's financial capital, housing the RBI, BSE, NSE, and the headquarters of all major Indian private sector banks that drive prepaid card program innovation.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

32.0% |

Government ministry prepaid card adoption, advanced digital payment infrastructure, highly organized sector workforce density. |

| West and Central India |

27.4% |

Role as a financial services hub, Large MSME industrial sector, Corporate enterprise base, IT and manufacturing corridor. |

|

South India |

24.1% |

IT/ITES workforce using neobank prepaid cards, manufacturing sector payroll card adoption, remittance-linked prepaid card use. |

|

East India |

16.5% |

Growing fintech adoption, government DBT program expansion, wage disbursement through prepaid instruments. |

South India's 24.1% share reflects the Bengaluru-Hyderabad IT corridor's technology-forward workforce and the region's strong neobank and fintech startup ecosystem, creating differentiated prepaid card products for tech-savvy consumers.

Competitive Landscape

The market is moderately concentrated. HDFC Bank Ltd., Axis Bank Limited, ICICI Bank Limited, and State Bank of India collectively hold the largest active prepaid card share.

|

Company Name |

Products |

Market Position |

Core Strength |

| HDFC Bank Ltd. | GiftPlus, E-GiftPlus, GiftPlus Corporate, Smarthub Vyapar, FlexiBenefit, MoneyPlus, Petty Cash Card |

Market Leader |

Largest private bank prepaid card issuance, corporate card management platform |

| Axis Bank Limited | Virtual Gift, Min-KYC Meal, Meal Card, Gift Card, Smart Pay Card | Co-Leader | Visa and RuPay prepaid card portfolio, contactless gift and travel cards, corporate payroll card programs |

| ICICI Bank Limited | PayDirect, Student Card, Umang | Co-Leader | iMobile Pay-linked prepaid cards, corporate prepaid, instant virtual card issuance |

| State Bank of India | Foreign Travel, eZ-PAy, Gift Card, Achiever, Mumbai Metro 3, GoSmart Agra Metro, SBI NMRC City1, Nagpur Metro Maha, SBI MMRDA Mumbai1, Singara Chennai, SBI Gosmart Kanpur Metro, Nation First Transit, HRTC - NCMC Prepaid | Strong Challenger | Largest bank branch network for prepaid distribution, RuPay prepaid portfolio, government DBT programs |

| Kotak Mahindra Bank Limited | Kotak FASTag, Forex, Gift Card, Kotak Spendz | Strong Challenger | Kotak zero-balance segment, tech-first customer experience |

Non-bank PPI issuers such as EbixCash and Pluxee India dominate specific corporate niches, while fintech-banking partnerships are creating new-generation prepaid products for digital-native segments.

Key Company Profiles

HDFC Bank Ltd.

HDFC Bank Ltd. is one of India's largest private sector banks and a market leader in prepaid card issuance. The bank offers travel forex cards, gift cards, corporate payroll cards, and general-purpose reloadable cards distributed through its branch network and digital platforms.

- Product Portfolio: GiftPlus Card, E-GiftPlus Card, GiftPlus Corporate Card, Smarthub Vyapar Card, FlexiBenefit Card, MoneyPlus Card, and Petty Cash Card.

- Strategic Focus: Digital-first prepaid card product innovation through PayZapp platform, forex travel card market leadership, corporate payroll card program expansion, and premium customer prepaid reward program development.

Axis Bank Limited

Axis Bank Limited is a leading private sector bank with a comprehensive prepaid card portfolio spanning consumer travel, gift, and corporate payroll programs, supported by Visa and RuPay network partnerships for broad merchant acceptance.

- Product Portfolio: Virtual Gift, Min-KYC Meal, Meal Card, Gift Card, and Smart Pay Card.

- Strategic Focus: Corporate gifting and incentive card market share growth, forex travel card innovation, fintech co-branded prepaid partnerships, and API-first corporate card program management platform development.

Market Concentration Analysis

India's prepaid cards market is moderately concentrated at the card issuance level. HDFC Bank Ltd., Axis Bank Limited, and ICICI Bank Limited collectively hold an estimated 45–55% of private bank-issued prepaid card value in circulation.

State Bank of India's largest branch network distribution base and Jan Dhan-linked prepaid card portfolio give it the largest absolute card count. Non-bank PPI issuers EbixCash and Pluxee India lead in specific corporate vertical niches but hold smaller overall market shares.

Investment & Growth Opportunities

Fastest Growing Segments

Open loop cards (~31.0% CAGR), government DBT prepaid programs, neobank-issued digital prepaid cards, and API-integrated corporate expense management platforms represent the highest-growth investment vectors through 2034, collectively addressing a combined incremental market of approximately USD 2.3 Trillion.

Emerging Market Expansion

Tier 2, 3, and 4 city markets represent the largest untapped consumer prepaid card opportunity, where rising smartphone penetration, improving digital payment literacy, and expanding e-commerce access are creating first-time digital payment users who are better served by prepaid cards than traditional bank accounts.

Venture and Institutional Investment Trends

- Indian fintech startups building neobank prepaid card platforms, including Fi Money, Jupiter, Niyo, and Slice have collectively raised over USD 1 Billion in venture capital, reflecting investor confidence in digital-first prepaid card business models serving India's growing millennial and Gen Z banking population.

- International payment networks Visa and Mastercard are actively investing in the Indian prepaid card ecosystem development through partnerships with Indian banks and fintech companies, providing technology, marketing, and go-to-market support for innovative prepaid card product launches.

Future Market Outlook (2026-2034)

India's prepaid cards market will reach USD 2,721.5 Billion by 2034 from USD 277.1 Billion in 2025, growing at an exceptional 28.9% CAGR driven by India's structural digital payment transformation. Open loop cards will consolidate their dominance as UPI interoperability expands universal acceptance.

India's prepaid card market will increasingly converge with UPI, CBDC (Digital Rupee), account aggregator data, and embedded finance APIs, creating personalized prepaid products that serve as comprehensive digital financial management tools beyond their original transaction-focused design.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 80 industry participants in 2024–2025, including bank prepaid card product managers, corporate card program operators, government DBT officials, fintech platform executives, and enterprise HR technology buyers across major Indian cities. Expert input validated market sizing, card type adoption trends, and regional dynamics.

Secondary Research

Secondary research encompassed RBI Payment System Reports, NPCI UPI and PPI transaction statistics, company annual reports, SEBI filings, fintech association reports, and trade publications, including Payments Cards & Mobile, Digital Transactions, and Financial Express's fintech coverage.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting, incorporating RBI PPI transaction data, card issuance volume estimates, average card balance, and transaction frequency assumptions, and vertical-specific adoption rate modelling. A base-case CAGR of 28.9% reflects the compounding impact of India's digital payment adoption curve, validated against RBI PPI statistical trends.

India Prepaid Cards Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Card Types Covered | Open Loop Cards, Closed Loop Cards |

| Purposes Covered | Payroll/Incentive Cards, Travel Cards, General Purpose Reloadable (GPR) Cards, Remittance Cards, Others |

| Verticals Covered | Corporate/Organization, Retail, Government, Others |

| Region Covered | West and Central India, South India, North India, East India |

| Companies Covered | HDFC Bank Ltd., Axis Bank Limited, ICICI Bank Limited, State Bank of India, Kotak Mahindra Bank Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Prepaid Cards Market Report

The market reached USD 277.1 Billion in 2025 and is projected to reach USD 2,721.5 Billion by 2034 at a 28.9% CAGR.

North India leads with a 32.0% share in 2025, driven by Delhi-NCR's corporate headquarters concentration and high digital payment adoption.

Open loop cards lead at 72.0% in 2025, leveraging Visa, Mastercard, and RuPay networks for universal merchant acceptance at POS terminals, ATMs, and e-commerce platforms.

Corporate/organization at 36.0% leads, driven by payroll card adoption for blue-collar workers, corporate travel expense management, and employee incentive programs.

HDFC Bank Ltd., Axis Bank Limited, ICICI Bank Limited, State Bank of India, and Kotak Mahindra Bank Limited are some of the key players.

UPI integration, the Digital India initiative, financial inclusion for the unbanked population, corporate expense digitization, and rising e-commerce adoption are primary drivers.

The Reserve Bank of India regulates prepaid cards as Prepaid Payment Instruments (PPIs) under the Payment and Settlement Systems Act 2007 and the Master Direction on Prepaid Payment Instruments (2021).

RBI-mandated PPI interoperability via UPI rails enables prepaid card balances to be transacted at 350+ million UPI-accepting merchant points, massively expanding prepaid card utility beyond traditional POS terminal acceptance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)